FusionWire, 2015.

Tapped in: The cashless tipping point is here

Tapped in: The cashless tipping point is here

For the first time, there’s a way to pay even easier than cash. We spoke to MasterCard and the UK Cards Association about how contactless is quickly becoming our favourite way to pay.

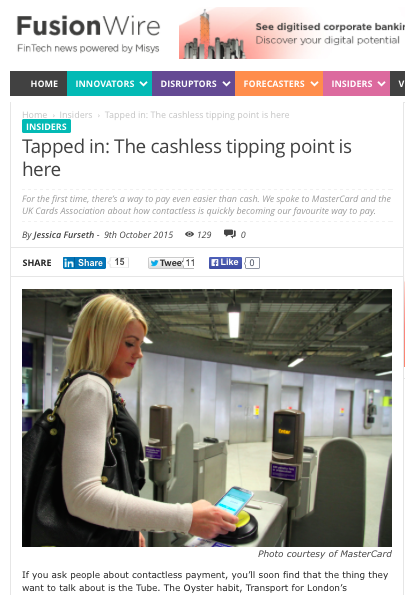

If you ask people about contactless payment, you’ll soon find that the thing they want to talk about is the Tube. The Oyster habit, Transport for London’s smartcard ticket that lets you tap in and out, has ensured a smooth transition to using our bank cards or mobile handsets in the same manner. Because getting people to change their behaviour isn’t just about making new technologies available to them – they have to want to use them.

“Contactless payments has been a slow burn for quite a few years in the UK, but in the last few years it’s really started to take off,” says Mike Cowen, European Head of Emerging Payments Products at MasterCard. The surge in contactless payments is far greater than can be explained just by more shops getting the kit to accept it, explains Cowen. This suggests the shift has just as much to do with culture: “We see a lot of people do their first contactless payment with Transport for London. It fits with the behaviours we’ve observed previously: there’s a barrier to overcome to do the first tap. But once they’ve done three or four, they tend to stick with it.”

Because if you’ve tapped in and out of the Tube, why not just tap to pay for a coffee on the way out of the station? It’s taken people a little while to realise how that little wave symbol on their card means they don’t have to use a PIN for small purchases, but there’s been a lot of noise around contactless lately. The arrival of Apple Pay has been particularly helpful, as people are now aware it’s possible to use a mobile handset to pay as well. “These things take on momentum,” says Cowen, explaining how you’ll always have the early adopters who jump in first. “But then you have a big chunk of the population, particularly around payment, who’re cautious around trying something new. But then they see other people doing it and that there’s no problem, and that builds their confidence.”

A method even easier than cash

By 2020, all end-of-sale payment terminals across the EU will be contactless-enabled, MasterCard has declared. This means we’re approaching an age when we may be able to say, for the first time, that there’s a payment method more convenient than cash: one single tap, and no need to make change or to get to an ATM. In the UK, we’re already taking to contactless with gusto: in the first half of the year, £2.5 billion was spent contactlessly – that’s more than we spent the whole of the year before, according to the UK Cards Association.

“The numbers reflect a growing awareness of the technology, and what it has to offer in terms of a really slick consumer experience,” says David Baker, head of the payment innovations unit at the UK Cards Association, the card payments industry trade body. “Contactless wins on speed and convenience, compared to other payment mechanics available at the point of sale.”

In September, the limit on contactless payments rose to £30 in the UK, meaning the spending volumes are likely to increase even more. Baker says the staggered increase in the limit has to do with caution as the industry learns: how the new technology works, and how it’s accepted by the consumer. Other countries, like the US and Australia, already allow higher contactless spending, suggesting we might see the UK limit rise again. Risk control has been another factor in the rollout of contactless, but so far, the system has proven reasonably robust, says Mike Cowen at MasterCard, pointing out that fraud on contactless is one of the lowest of any kinds of payment: “We’re always concerned about fraud, but at the moment, the industry is doing a pretty good job at managing it. That applies in particular to contactless.”

Towards the cashless society

While financial organisations have an economic incentive for driving more payments through electronic channels, there are arguably good reasons why this shift could be a positive factor for society at large. The cost of cash ranges from 0.5% to 1.5% percent of GDP, depending on the country, according to research from MasterCard. Cash-intensive economies are less productive per capita, MasterCard concluded in a 2012 paper, which found a correlation between countries with high cash use and problems like fraud and bribery, not to mention how people often favour cash when they don’t trust their governments.

But even in the UK, where most people use electronic payments, we’re still very fond of notes and coins. 48% of UK money transactions were cash-based last year, according to the Payments Council. (The organisation is now part of Payments UK.) This is the first time electronic payments via cards or transfers have overtaken cash in the UK. The Payments Council said it expects cash volumes to fall by 30% over the next 10 years, as increasing use of contactless and mobile payments are driving the trend.

“Cash has been around for thousands of years, and it’s ingrained in our society,” says David Baker at the UK Cards Association. “Just like the cheque is difficult to get rid of, cash will take a long, long time to disappear. Those over 50 are probably more wedded to cash, but my kids – the millennials – they’re not that bothered by cash, and make payments to their mobile phones quite naturally nowadays. But it’s going to be a generation or two, before we ever reach that truly cashless society.”

Innovations in cashless technology

Only 4.4% of people in the UK go so far to rarely use any cash at all, according to the Payments Council. One reason for this is probably because there are still lots of places that remain cash-only: small shops, certain pubs, car boot sales, the dog walker. The cost of implementing cashless technology can be a significant barrier: “Back when we implemented chip and PIN, there was an enormous cost of upgrading points-of-sale to accept chipped cards,” says Baker. But the move towards contactless has been a lot simpler: “With contactless, only a few years later, the technology was already there: essentially all you had to change was the reader.”

Spending a day without cash is becoming easier now that small retailers are increasingly accepting cards – in the past they’ve often held out due to cost. “There’s been a lot of innovation around that in recent years,” says Mike Cowen at MasterCard. mPOS (mobile point-of-sale) devices have become popular with small businesses; these are typically small, low cost payment terminals which don’t have communication capabilities built into the device itself, but instead connect to a mobile phone. “They tend to be inexpensive, and packaged in such a way that the point of entry is very affordable for small businesses,” says Cowen, explaining how the the cost of accepting card payments depends on the agreement between the retailer and their bank. “Extending the reach of card payment is probably the most critical thing for moving towards a cashless society.”

Both Cowen and Baker consider the rising number of choices when it comes to payment methods to be a good thing, as it increases awareness and boosts competition. “Payments is not a one-size-fits-all world. People have different preferences,” says Cowen. Baker is in shares this sentiment, but believes we’ll eventually see some consolidation: “We’ll probably start to see some of the mobile phone apps converge. As consumers, you don’t want eight different payment mechanics on your device. That’s confusing for you, and for the retailer. … But you need innovation to spark off interest, and get things moving.”